Top Industries Driving Vertical SaaS Growth

Top Industries Driving Vertical SaaS Growth

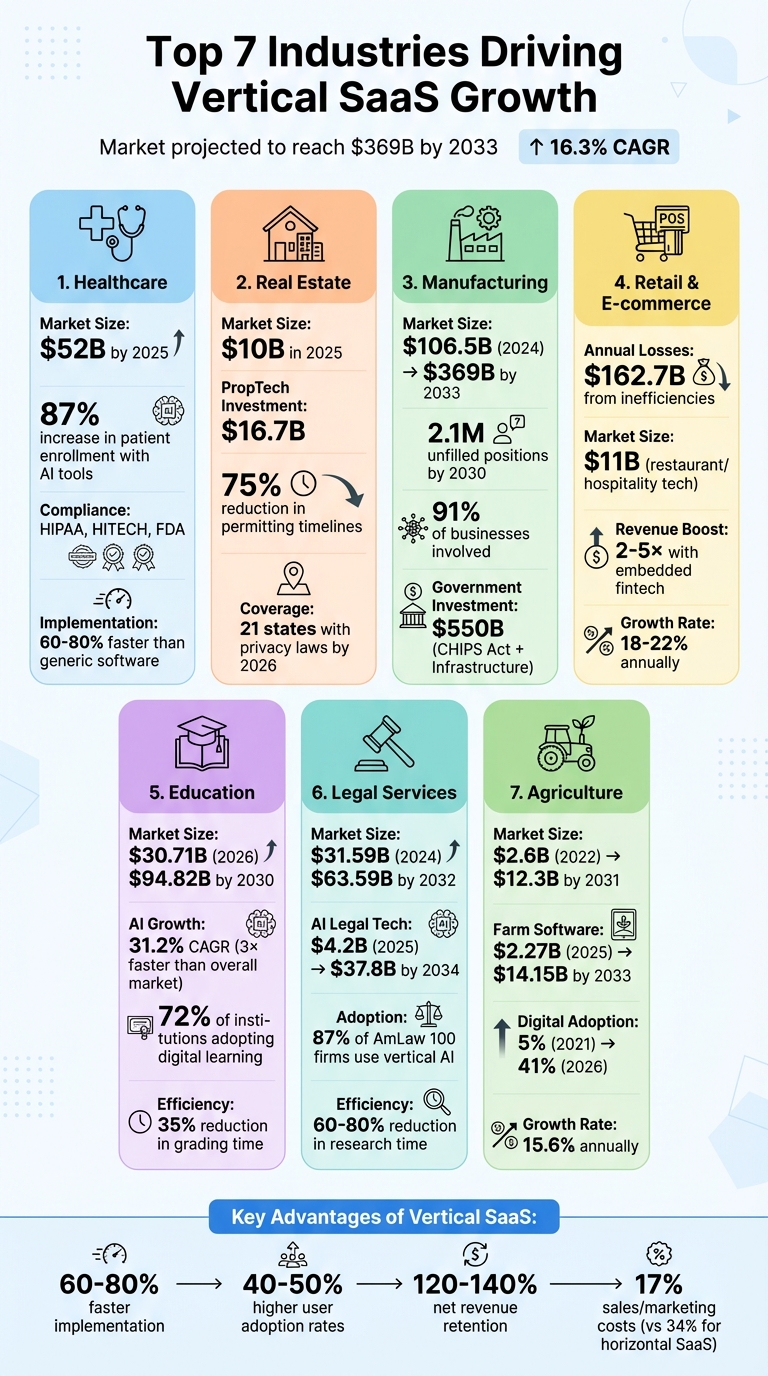

Vertical SaaS is transforming industries by offering software tailored to specific needs, unlike general-purpose tools. With a projected market value of $157 billion by 2025, this sector is growing faster than horizontal SaaS, fueled by demand for industry-specific features, regulatory compliance, and workflow integration. Here's a quick look at the leading sectors driving this growth:

- Healthcare: Compliance with HIPAA, HITECH, and FDA regulations, seamless EHR integration, and tools like AI-driven patient financing platforms.

- Real Estate: Solutions for managing MLS agreements, privacy laws, and financial operations; platforms streamline complex transactions and compliance.

- Manufacturing: Tools like MES and QMS manage production lines, IoT integration, and supply chains, addressing labor shortages and operational challenges.

- Retail and E-commerce: Industry-specific tools like POS systems and embedded fintech, reducing inefficiencies and boosting operational margins.

- Education: Platforms like Canvas LMS and PowerSchool automate grading, compliance reporting, and student data management.

- Legal Services: AI-powered tools for contract analysis, billing, and compliance with regulations like GDPR and the EU AI Act.

- Agriculture: Farm management software integrates financial tools, traceability, and ESG compliance for efficient operations.

Vertical SaaS offers faster implementation, higher adoption rates, and lower customer acquisition costs, making it the preferred choice for businesses with unique workflows and compliance needs.

7 Industries Driving Vertical SaaS Growth: Market Size and Key Statistics

1. Healthcare

Industry-specific compliance requirements

The healthcare industry operates under some of the most demanding regulatory standards, making compliance a top priority for Vertical SaaS platforms. These platforms must incorporate safeguards like HIPAA and HITECH to protect patient data, adhere to HL7 and FHIR standards to ensure interoperability across systems (like electronic health records and pharmacy platforms), and secure FDA approval for Software as a Medical Device (SaMD) when offering diagnostic or treatment capabilities. Meeting these requirements involves implementing advanced security protocols, which create significant hurdles for generic software attempting to compete in this space.

Compliance isn’t a one-time effort - it requires ongoing commitments. Healthcare providers must execute Business Associate Agreements (BAAs) to manage protected health information legally. On top of that, initial investments for HIPAA compliance and HL7 integration can range from $50,000 to $200,000, with an additional $20,000 to $80,000 annually needed for audits. Concerns over data sovereignty have also made HDS-certified sovereign data centers a standard for SaaS migrations, with many providers opting for "Cloud-Light" managed services instead of fully public cloud solutions. These high compliance demands are driving a wave of transformation in healthcare IT.

Adoption of digital transformation

The healthcare IT market is on a steep growth trajectory, projected to hit $52 billion by 2025. Meanwhile, the broader healthcare software market, valued at $38.5 billion in 2026, is expected to surpass $100 billion by 2035 with a compound annual growth rate of 10.34%. This reflects a robust shift toward cloud-native platforms designed to meet intricate regulatory and clinical requirements.

Investment in digital health solutions has surged, with $9.9 billion raised by Q3 2025, and AI-focused solutions capturing 62% of the funding. For example, PayZen secured $232 million in late 2024 to expand its AI-driven patient financing platform. This funding led to an 87% increase in patient enrollment and a 40% improvement in payment collections for healthcare providers. Similarly, Abridge, which focuses on automating medical notes, raised $250 million in 2025, bringing its valuation to $5.3 billion. The company now partners with over 150 U.S. health systems to reduce administrative burdens.

Complex workflows requiring tailored solutions

Regulatory requirements may push technology adoption, but healthcare’s intricate workflows demand solutions that fit seamlessly into clinical operations.

"Domain expertise - knowing how a vet thinks or how a pharmacist dispenses - is proving more valuable than the underlying code".

Vertical SaaS platforms cater to these needs with specialized tools like drug dosage calculators, SOAP notes, and animal-specific health record formats. These prebuilt features allow for 60–80% faster implementation and boost user adoption rates by 40–50% compared to generic software.

The move from outdated, monolithic systems to modular platforms is revolutionizing healthcare operations. Modern Vertical SaaS automates data retrieval using FHIR APIs instead of manual processes like faxing, applies predictive analytics rather than rigid rule-based workflows, and adopts cost-effective annual subscription models. These tailored solutions are making a real difference:

- 50% reduction in clinician burnout by automating administrative tasks

- 90% fewer clinical data errors through robust EHR/EMR integration

- 40% drop in patient no-shows and 60% faster claims processing

One standout example is Apella Technology, which raised $80 million in January 2026 to expand its AI sensor platform. This system integrates with surgical SaaS to improve data accuracy and outcomes in operating rooms.

2. Real Estate

Industry-specific compliance requirements

Real estate platforms have to navigate a complex web of regulations that vary widely by state. By 2026, 21 states will enforce consumer privacy laws, covering nearly half of the U.S. population. New laws in states like Delaware, Iowa, New Hampshire, New Jersey, Tennessee, Minnesota, Maryland, and Kentucky are set to take effect in 2025, adding to an already fragmented regulatory environment. For platforms operating across multiple states, this means managing varying rules on opt-out options, data retention, and consumer rights.

"A real estate platform with users across multiple states is almost certainly subject to privacy obligations beyond CCPA, and the specific requirements... vary meaningfully across states." – GTC Systems

But it’s not just privacy laws. Real estate SaaS providers also have to comply with MLS access agreements, which come with their own display and data retention rules. Platforms facilitating large transactions face FinCEN’s anti-money laundering (AML) requirements, while those handling payments must adhere to PCI DSS standards. On top of that, the EU AI Act, which began phased enforcement in 2025, affects AI systems used for tasks like automated valuation models, tenant screening, and lead scoring. For platforms serving institutional clients, achieving SOC 2 Type II certification has become almost mandatory. Compliance automation tools like Vanta or Drata help with this but come at a cost - ranging from $15,000 to $40,000 annually. These regulatory hurdles are pushing the real estate industry toward more advanced digital solutions.

Adoption of digital transformation

By 2025, the real estate technology market hit roughly $10 billion, reflecting a major shift in how the industry operates. That same year, PropTech investments reached $16.7 billion, with institutional investors leading one in three seed rounds.

"PropTech now hinges on the systems managing capital, construction, and financial operations." – Ashkán Zandieh, Founder and Managing Director at the Center for Real Estate Technology & Innovation

This digital transformation is partly driven by changing demographics. Millennials now make up 43% of all homebuyers, and 75% of them see digital tools as critical for business success - compared to just 49% of Generation X. Meanwhile, private equity firms are consolidating smaller, independent businesses into larger, more efficient operations. This evolution demands platforms that can handle increasingly complex operational needs.

Complex workflows requiring tailored solutions

The real estate industry deals with intricate workflows involving multiple parties. Generic software often falls short, which is why vertical SaaS platforms have become essential. These platforms streamline financial management, compliance, and audit trails, making them indispensable for real estate operations.

For example, in February 2026, Loft47 introduced a tool that automates deal creation and compliance reviews by extracting data from PDFs. Similarly, GreenLite’s AI-driven plan review system, launched in January 2026, cut permitting timelines by up to 75%. In 2025, Vantaca raised $300 million to expand its platform, which centralizes payments, receivables, accounting, and compliance for community associations. Arch also secured $52 million to automate treasury workflows, rent collection, and investor reporting for real estate portfolios. Compass has developed a vertical SaaS platform tailored for real estate brokerages, integrating transaction management and CRM to replace generic tools with solutions designed specifically for real estate workflows.

These platforms often achieve high switching costs due to their deep integration into daily operations. Many top-tier companies report net revenue retention (NRR) rates exceeding 120%, underscoring the value of these specialized solutions.

3. Manufacturing

Adoption of digital transformation

The manufacturing industry is moving away from outdated, paper-based processes and embracing modern cloud platforms. Today, 91% of businesses are involved in some form of digital initiative, and 87% of senior business leaders rank digitization as a top priority.

"Manufacturing was largely bypassed by recent software innovation waves, and represents another significant opportunity." – Activant Capital

However, the U.S. manufacturing sector is grappling with a labor shortage, with projections showing 2.1 million unfilled positions by 2030. This challenge stems from skill gaps and an aging workforce. Government initiatives like the CHIPS and Science Act and the Bipartisan Infrastructure Law are accelerating modernization efforts. With $550 billion allocated for construction and manufacturing projects, companies are being pushed to reshore production and upgrade operations. SaaS platforms are stepping in to help manufacturers maintain efficiency despite workforce limitations. These tools also provide better control over increasingly complex supply chains, making them indispensable as the industry digitizes.

Complex workflows requiring tailored solutions

Manufacturing workflows are unlike those in other sectors. The software used here is not just a data tracker - it’s a "System of Consequence", meaning if the software fails, production halts. These platforms act as the operational brain, connecting to IoT sensors on factory floors to oversee production lines and manage material flow in real time.

"If this software fails, the work stops." – Artis Bisers, Investment Manager, Vendep

Generic tools often fall short in handling this complexity. Manufacturers require specialized platforms, such as Manufacturing Execution Systems (MES) for production oversight, Enterprise Asset Management (EAM) for predictive maintenance, and Quality Management Systems (QMS) to ensure regulatory compliance. Modern platforms are designed with modular architectures, enabling manufacturers to add new features - like warehouse analytics or advanced scheduling - without disrupting existing systems.

Companies like Tulip Interfaces and Instrumental are leading the charge. Tulip offers no-code apps that digitize shop-floor operations, while Instrumental leverages AI to detect and resolve product issues in real time during the manufacturing process. Once these platforms are integrated with physical hardware, they create high switching costs, making them indispensable to daily operations. This deep integration also drives strong revenue retention and positions the industry for significant growth.

Market growth potential for SaaS

These specialized systems not only streamline production but also open up enormous market opportunities. The global vertical SaaS market is expected to grow from approximately $106.5 billion in 2024 to over $369 billion by 2033, with an annual growth rate of 16.3%. Manufacturing finds itself in a prime position - while the industry has adopted some technology, there’s still plenty of room for modernization.

The business model for these platforms is also evolving. Instead of traditional per-seat licenses, manufacturers are transitioning to outcome-based pricing, where costs are tied to units produced or shipped rather than the number of users. This shift aligns with the rise of embedded fintech, a market projected to hit $3.6 trillion by 2030. By addressing long-standing compliance and operational challenges, these innovations are driving sustained demand for specialized SaaS solutions tailored to manufacturing needs.

4. Retail and E-commerce

Complex Workflows Requiring Tailored Solutions

Retail operations come with their own set of challenges that generic software just can’t handle. Take a restaurant, for example - it might need to update menu items on the fly, split bills by seat, or sync inventory across multiple locations. These are tasks that horizontal tools, like standard CRMs or spreadsheets, weren’t designed to manage. As a result, retailers often end up relying on manual workarounds, which can be both time-consuming and costly.

Vertical SaaS platforms step in by offering solutions tailored specifically to these industry needs. They integrate functions like point-of-sale (POS), inventory management, and supplier coordination into one seamless system. In fact, tools like POS systems, e-commerce platforms, and scheduling software now account for 29% of all primary vertical SaaS products. This kind of specialized functionality not only boosts efficiency but also creates high switching costs, making it harder for customers to move to a competitor.

"Think of it this way: horizontal SaaS builds a hammer. Vertical SaaS builds the exact tool a roofer needs to install a specific type of shingle." – Anika Tabassum Nionta, Content Manager, Ellty

By addressing these unique needs, vertical SaaS helps streamline retail operations and accelerates the sector’s shift toward digital transformation.

Adoption of Digital Transformation

The retail industry is under pressure to tackle operational inefficiencies, and SaaS adoption is becoming a key driver of change. Retailers lose a staggering $162.7 billion annually due to in-store inefficiencies - a 27% increase from 2024. These losses now make up 5.5% of gross sales, with 81% of retailers seeing at least a 5% hit to their operating margins.

To combat these issues, companies are turning to advanced technologies. For instance, ShopRite introduced Simbe’s autonomous Tally robot in June 2025. The results? A 50% drop in out-of-stock items at high-volume locations, 98% on-shelf availability, and a 90% improvement in pricing accuracy. Investments in store intelligence tools have skyrocketed by 151% year-over-year as retailers realize the cost of falling behind.

Market Growth Potential for SaaS

The efficiency gains from SaaS adoption are just the tip of the iceberg - retail is also primed for major market growth. The restaurant and hospitality tech market alone reached an estimated $11 billion in 2025. Across the board, vertical SaaS is growing at an annual rate of 18–22%, outpacing the 12–15% growth of horizontal SaaS. A great example is Shopify, which reported 27% year-over-year growth in Q1 2025, bringing in $2.36 billion in quarterly revenue through its integrated e-commerce, payments, and financial services offerings.

One standout trend is the rise of embedded fintech. Today, 87% of vertical SaaS companies with fintech capabilities include payments in their offerings. This approach can boost revenue per customer by 2–5× compared to traditional subscription models. But payments are just the beginning - platforms are now adding lending, insurance, and cards directly into their systems. Interestingly, 41% of companies that start with a Commerce or Front Office product eventually expand into fintech services. This diversification creates multiple revenue streams and deepens their integration into customers’ daily operations.

5. Education

Complex Workflows Requiring Tailored Solutions

Educational institutions often juggle administrative tasks that are too intricate for off-the-shelf software. Teachers spend hours grading assignments, administrators face hurdles with state compliance reporting, and IT teams manually sync student rosters across various applications. These tasks are far too specialized for generic tools like spreadsheets or basic CRMs to handle effectively.

Vertical SaaS platforms are stepping in to solve these issues. Take Canvas LMS, for example - it uses AI-powered SpeedGrader technology, cutting teacher grading time by nearly 35% compared to traditional methods. Similarly, PowerSchool SIS automates tasks like master scheduling and compliance reporting, saving administrators countless hours. Tools like Clever streamline operations by acting as a single sign-on bridge, automatically syncing student data across apps and saving IT departments thousands of hours of manual work. These platforms don't just digitize existing processes - they completely reshape how schools operate by embedding industry-specific workflows directly into their software.

Adoption of Digital Transformation

The education sector is leaning heavily into digital tools to tackle long-standing challenges. A striking 72% of educational institutions point to the growing demand for digital learning as the main reason for adopting EdTech. This shift isn't just about replacing paper with screens - it's about reimagining how education functions. By late 2025, 72% of higher education institutions were expected to be using or testing AI-driven personalized learning tools.

The impact is undeniable. AI-powered adaptive tutoring has been shown to improve learning outcomes by 4.1x compared to traditional one-size-fits-all curriculums. Predictive analytics are also making waves; "Early Warning" systems can identify at-risk students 8–12 weeks before potential issues arise, enabling proactive interventions . Beyond the classroom, tools like Remind help bridge the communication gap between schools and families, offering auto-translation in over 90 languages to keep non-English-speaking parents informed. These advancements are not just transforming educational practices - they’re driving significant growth in the EdTech market.

Market Growth Potential for SaaS

The education software market is experiencing explosive growth. It surged from $24.89 billion in 2024 to a projected $30.71 billion by 2026. Looking further ahead, the global market for education technology SaaS tools is expected to hit $94.82 billion by 2030, with a CAGR of 14.1% between 2024 and 2030. Even more striking, AI-powered education software is growing at a blistering 31.2% CAGR - three times faster than the broader market.

This isn't just theoretical growth. In April 2024, Ellucian Company L.P. introduced Ellucian Intelligent Processes (EIP), a no-code SaaS solution that automates workflows across Finance, HR, and Registrar departments. Just two months later, D2L Corporation acquired H5P Group, adding over 60 interactive content types to its platform to enhance content creation. Many platforms are also diversifying revenue streams - 88% of companies using embedded finance tools report higher engagement, generating new income through payment processing and other financial services. With top vertical SaaS companies in education boasting net revenue retention rates of 120-140%, it’s clear that once schools adopt these platforms, they’re in it for the long haul.

6. Legal Services

Industry-Specific Compliance Requirements

The legal industry operates under some of the most stringent compliance standards, which has fueled the adoption of specialized SaaS tools. For instance, under the EU AI Act, legal AI tools used in areas like contract enforcement or dispute resolution are deemed high-risk. These tools must adhere to strict guidelines, including mandatory human oversight, detailed technical documentation, bias monitoring, confidence indicators, and an override feature to ensure attorneys retain control. Additionally, data privacy laws like GDPR and CCPA require platforms to incorporate features such as data residency controls and workflows for the right to erasure. Between 2024 and 2025, state bar associations introduced guidance mandating attorneys to ensure AI-assisted tasks are explainable. On top of this, SOC 2 Type II certification has become a baseline security benchmark for vendors. These complex regulatory demands highlight the need for tools that can simplify and support intricate legal operations.

Complex Workflows Requiring Tailored Solutions

The intricate workflows of legal practice often render generic software inadequate. Attorneys juggle tasks like drafting documents, tracking billable hours, managing cases, handling trust accounting, and communicating with clients - needs that require specialized solutions. Vertical SaaS platforms meet these challenges by embedding AI directly into legal practice management systems. For example, Smokeball's Autotime feature uses AI to track computer activity and automatically convert it into billable time, adding an average of 30+ additional billable minutes daily. Harvey, a platform valued at $11 billion with $190 million in annual recurring revenue as of February 2026, serves a majority of AmLaw 100 firms by automating tasks like contract analysis and compliance. Similarly, EvenUp, valued at $2 billion in October 2025, focuses on personal injury cases, automating demand package assembly and processing 10,000 cases weekly, with over 200,000 cases resolved to date.

Law firms are also consolidating their tech tools to minimize the hassle of managing multiple subscriptions. Platforms like CosmoLex and MyCase Pro provide all-in-one solutions. CosmoLex, priced at $109 per user per month, and MyCase Pro, at $89 per user per month, combine essential features like double-entry accounting, AI-assisted writing, and document management into a single interface.

"Consolidation beats specialization when the cost of context-switching exceeds the value of optimization".

Market Growth Potential for SaaS

The legal tech market is experiencing rapid expansion. In 2024, it reached $31.59 billion and is projected to grow to $63.59 billion by 2032, with a 9.4% compound annual growth rate (CAGR). Vertical AI tailored for legal services is growing even faster, valued at $4.2 billion in 2025 and expected to hit $37.8 billion by 2034, reflecting an impressive CAGR of 28.5%. Legal practice management software alone is forecasted to reach $5.96 billion by 2032.

Adoption rates are climbing across firms of all sizes. By Q1 2026, 87% of AmLaw 100 firms had enterprise agreements with at least one vertical AI platform. Mid-sized firms using tools like Harvey have reported productivity boosts of 35%. AI-driven workflows are cutting legal research time by 60–80% and slashing document review costs from $1.50–$2.50 per document to under $0.15. Between 2022 and 2025, Fortune 500 corporate legal departments reduced outside counsel spending by an average of 12.4% by shifting work to AI-powered in-house tools.

Investment in legal tech is also surging. Venture capital funding rebounded to $2.6 billion across 164 deals in 2024. Vertical SaaS companies in this space report net revenue retention rates between 120% and 140%, underscoring strong customer loyalty and high switching costs.

7. Agriculture

Industry-Specific Compliance Requirements

The growth of vertical SaaS in agriculture mirrors trends in industries like healthcare and real estate, where compliance and specialized solutions are key drivers. Agriculture, in particular, requires software that meets its unique regulatory and operational demands.

Take food safety standards, for instance. Regulations such as FSSAI necessitate platforms that can manage detailed data and ensure compliance from the ground up. Similarly, "farm-to-fork" traceability relies on secure, unchangeable records throughout the supply chain. In Europe, strict ESG regulations demand tools for real-time carbon tracking and monitoring environmental data. Export markets also require digital compliance systems to verify product origins and meet international standards, which are critical for accessing premium buyers. Vertical SaaS platforms excel here by embedding compliance into their core design rather than treating it as an add-on.

Adoption of Digital Transformation

Agriculture is undergoing a major digital transformation, moving from basic spreadsheets to intelligent, AI-driven platforms that streamline operations. The numbers tell the story: digital technology adoption on farms jumped from 5% in 2021 to a projected 41% by 2026, with large farms (over 5,000 acres) expected to hit 81% adoption.

The industry is shifting beyond traditional ERPs to embrace advanced "Systems of Action." These platforms not only process orders but also provide recommendations and autonomously manage logistics.

"Software companies that embed AI deeply into industry-specific workflows will capture disproportionate value moving forward and empower businesses like crop input retailers to win." - Shane Thomas, Upstream Ag Professional

This evolution demands software that directly addresses the unique challenges of agricultural operations.

Complex Workflows Requiring Tailored Solutions

Agriculture's unique challenges - like seasonal labor, unpredictable weather, and intricate crop cycles - often exceed the capabilities of generic CRM tools. For example, farmers need edge computing to analyze data locally on devices like drones or sensors when internet access is limited. These systems sync with the cloud once connectivity is restored.

Modern AgSaaS platforms go even further by integrating financial tools such as crop insurance APIs, lending services, and credit risk profiling directly into farm management software. This integration has been shown to boost revenue and retention by 2–5×. Yet, only 22% of farmers report being "very satisfied" with their current software, highlighting the need for more tailored solutions.

Market Growth Potential for SaaS

The Agriculture Technology-as-a-Service market is on a steep growth trajectory, projected to grow from $2.6 billion in 2022 to over $12.3 billion by 2031. Farm management software alone is expected to rise from $2.27 billion in 2025 to $14.15 billion by 2033, reflecting an annual growth rate of 15.6%.

Vertical SaaS companies in agriculture often achieve net revenue retention rates above 130%. In 2025, AgTech funding reached roughly $2.3–$2.4 billion, with a focus on validation and efficient scaling. Subscription costs for specialized tools typically range from $50 to $300 per month. Additionally, blockchain-based traceability adoption is forecasted to hit 53% by 2026, underlining the sector's embrace of cutting-edge technology.

Why Vertical SaaS Is Winning In 2025

Conclusion

Vertical SaaS is reshaping industries like healthcare, real estate, manufacturing, retail, education, legal services, and agriculture. These sectors are turning to specialized software because generic tools fall short of handling their unique workflows, regulatory requirements, and operational challenges. The numbers back this up: vertical SaaS boasts higher retention rates while keeping sales and marketing expenses at just 17% of revenue, compared to 34% for general-purpose vendors.

The appeal lies in features tailored to specific industries. For example, healthcare platforms integrate seamlessly with EHR systems and meet HIPAA standards, real estate software connects directly to MLS databases, and manufacturing tools sync with IoT asset tracking systems. These specialized integrations lead to 60–80% faster implementation times and 40–50% higher user adoption rates, outperforming the customization of horizontal software.

This shift is not only driving industry growth but also creating diverse career opportunities. Companies in vertical SaaS need experts in sales, AI, embedded finance, and customer success to cater to industry-specific demands. There’s also a rising need for compliance specialists who can navigate regulations like HIPAA or SEC guidelines. As Rebecca Rodseth and Richard Benson-Armer of Activant Capital explain:

"We believe the future of software is vertical, which is resulting in a reshaping of the software industry, creating significant opportunities for both established players and innovative startups alike".

The growth potential in vertical SaaS is enormous. The market is expected to expand from $157 billion in 2025 to over $369 billion by 2033. For professionals, this means a chance to lead change by building deep domain expertise. Understanding specific workflows - like how construction accounting or medical billing operates - can give you a major advantage in this rapidly evolving space.

To fast-track your career in vertical SaaS, consider seeking mentorship from experienced Go-to-Market leaders. Platforms like Stackd can connect you with experts who provide personalized guidance in sales, customer success, marketing, and product strategy - skills that are invaluable when addressing the unique needs of vertical markets.

FAQs

How do I pick the right vertical SaaS industry to focus on?

To pick the best vertical SaaS industry, start by looking at growth potential and funding trends in fields like healthcare, real estate, or construction. Dig into the unique challenges each industry faces - like complex workflows or regulatory requirements - to spot opportunities where customized SaaS solutions can thrive. Finally, prioritize industries with unmet needs or areas where you already have domain expertise, as this can give you a stronger edge in building a successful product.

What integrations matter most when adopting vertical SaaS?

For vertical SaaS, the most impactful integrations are those designed to fit the unique workflows, compliance requirements, and operational processes of a specific industry. These integrations help build a connected ecosystem that simplifies tasks, boosts efficiency, and supports the specialized needs of each sector.

How should vertical SaaS vendors handle compliance without slowing releases?

Vertical SaaS vendors can stay compliant without slowing down their release cycles by weaving industry-specific regulatory requirements directly into their development processes. This approach ensures that compliance becomes a natural part of the workflow rather than an afterthought. Additionally, conducting regular certifications and security audits is crucial. These practices help maintain compliance standards while allowing development teams to keep their release schedules on track.